Introduction

In December of 2023, the Token Engineering Commons migrated its $TEC token infrastructure from Gnosis Chain to Optimism Mainnet. This was a strategic decision that intended to bring greater visibility, easier access, and stronger alignment with the work of the TEC.

After a year and a half, we are taking a moment to begin a discussion and to evaluate the Token Infrastructure. The migration is complete, we’ve implemented a new ABC page, and the fundamental infrastructure for the TEC economy has been deployed. However, there are still important questions that remain. How strong is the $TEC token economy? Where are the pain points and vulnerabilities? What parts of the system are working as intended and which areas are lagging behind? More importantly, what are the next steps that will allow us to evolve, adapt, and grow the value of this token and the Commons it represents?

This document serves as an initial diagnostic report and a strategy proposal designed to help $TEC token holders understand the current architecture and participate in decisions that will shape the next chapter for the $TEC token economy.

$TEC Supply & Distribution (July, 2025)

Before we can evaluate how $TEC is functioning in markets or funding mechanisms, it’s important to start with the fundamentals. The token supply, holder base, and asset backing form the foundation of the economy we are trying to manage. This section provides a snapshot of the $TEC token’s current footprint, including its supply metrics and the structure that gives it intrinsic value.

-

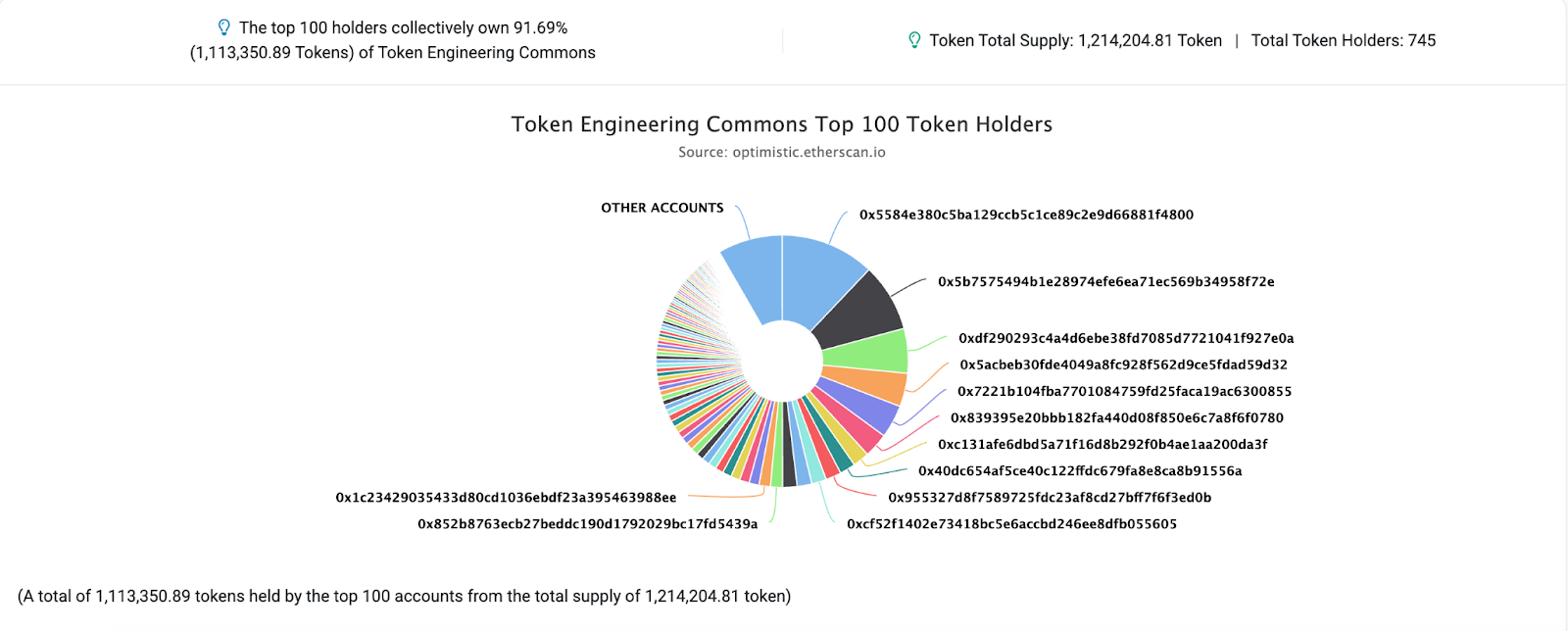

Total Supply: 1,214,204.81 $TEC

-

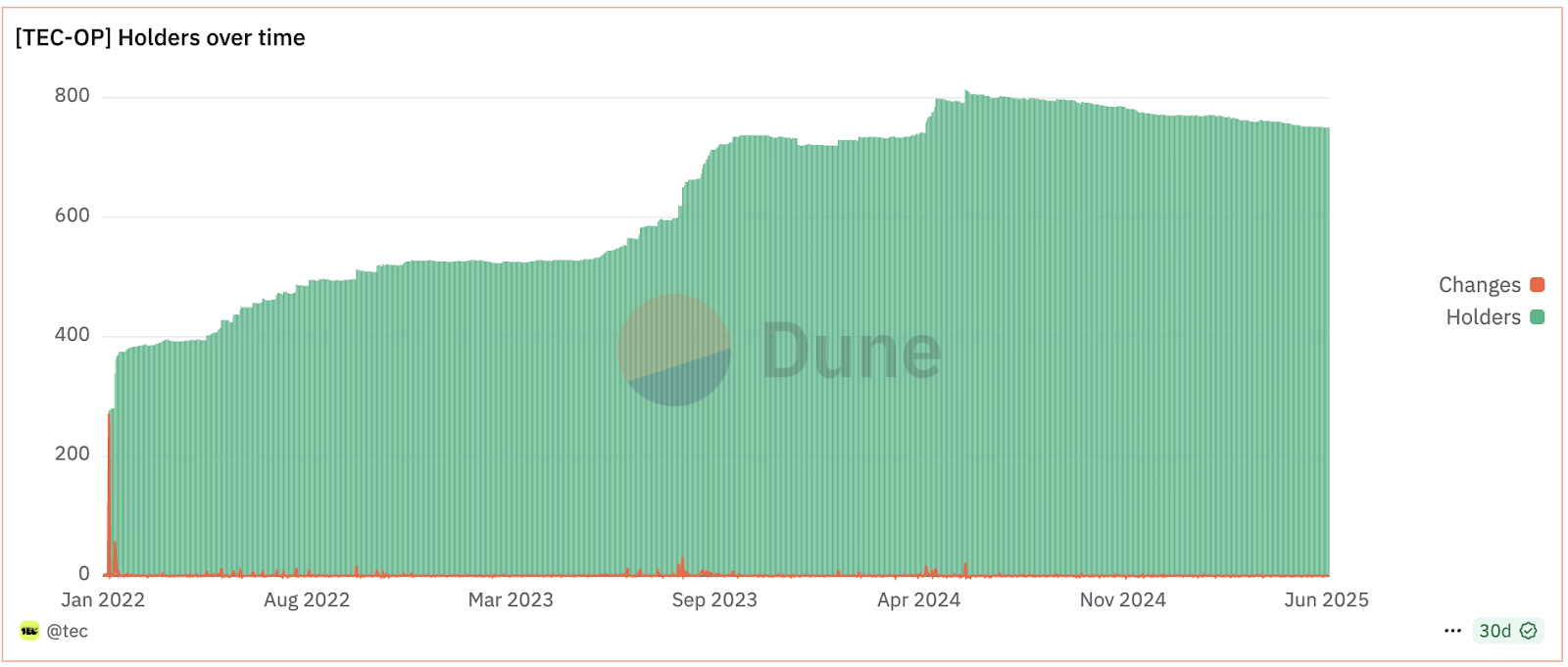

Token Holders: 745 ~(and growing)~ [Growth is not an accurate representation. Thank you @Rex for highlighting this mistake]

-

Network: Optimism Mainnet

-

Token Contract Address: 0x8Fc7C1109c08904160d6AE36482B79814D45eB78

-

Common Pool Address: 0xB941365430A16659658bb23B88eFAede1D839354

-

Reserve Pool Address: 0xae34eb7c3163aAD32142fbBCf15EC234c9EF173f

Token Holders

Tracking the number of token holders is one of the clearest indicators of community growth and network reach. Each unique holder represents a potential contributor, user, or advocate who has a stake in the TEC and may engage in governance, participate in funding, or help expand the ecosystem. A healthy and steadily growing holder base reflects confidence in the project’s mission and infrastructure, while sudden drops or concentration in a few wallets may signal risk or disinterest. Monitoring this metric over time helps us assess adoption, decentralization, and readiness for broader participation.

While the majority of $TEC tokens are held by the top 100 token holders (90% of all $TEC), the token holder growth chart reveals a clear trendline of consistent adoption post-migration. Notably, the transition to Optimism did not disrupt participation, but rather it expanded the distribution of $TEC and attracted new wallets to the ecosystem. [This is a false representation, see comments below]

As the number of token holders continues its path, it becomes increasingly important for TEC to maintain an active relationship with this base. Moving forward, we intend to develop clearer channels for engaging with holders more regularly, sharing key updates, and inviting participation in governance activities.

Augmented Bonding Curve (ABC)

With a basic understanding of the token’s distribution, we can now explore the core mechanism that governs its issuance and redemption through the Augmented Bonding Curve. This section outlines how it works, the funding it’s generated to the Common Pool since migration, and why the tribute system is central to its design.

The Augmented Bonding Curve (ABC) is the primary financial mechanism behind the $TEC token infrastructure. It is a programmable price curve that governs token minting and redemption. Users buy $TEC at a rising price, and sell $TEC back to the curve at a decreasing price. For each buy and sell a small percentage of value is routed to our collective treasury, the Common Pool. The Common Pool funds the TEC’s infrastructure, grants, and operations.

Reserve Pool

Every $TEC token minted through the Augmented Bonding Curve is backed by a share of our reserve asset, which is currently held in $rETH, a liquid staking derivative of Ethereum.

$rETH is a volatile, yield-bearing asset, and is a departure from our wxDAI reserve asset backing the ABC on Gnosis Chain. Our current reserve asset tracks the price of ETH and it accrues staking rewards over time. This means the Reserve Pool not only fluctuates with the broader crypto market, but also grows passively. As the reserve appreciates, so does the underlying value of $TEC.

This setup makes $TEC more than just a governance token. It functions as a synthetic ETH-linked asset with built-in exposure to Ethereum’s staking economy. It’s a powerful design, but one that comes with risk. Volatility in the price of $ETH, and the security of $rETH is inherited by $TEC, and maintaining trust in the token requires active awareness for both price and security.

Ultimately, the Reserve Pool is what ties $TEC to real economic value. It anchors the token to a productive asset and gives us a foundation to build a more resilient and regenerative economy for the Commons moving forward.

Common Pool & Reserve Pool (July 2025):

Currently, the Common Pool holds ~200k in assets including DAI, rETH, and TEC. The current breakdown of the Common Pool and Reserve Pool are listed here:

| Pool | Value | Assets |

|---|---|---|

| Common Pool | $207,215.42 | 154,214.17 DAI; 16.63 rETH; 1,587 TEC |

| Reserve Pool | $42,775.13 | 13.32 rETH |

As we move forward with our funding proposal for H2, we should look into moving some of our Stables into productive assets like rETH, and stETH to caputre the upside of potential value accrual to $ETH in the coming year.

ABC Tributes

To fully understand the impact of the bonding curve, we need to look at tributes. Tributes are designed incentives that feed the Common Pool, which creates economic sustainability for the Commons. The purpose and importance of setting tributes within the $TEC economy is critical to long-term viability.

Current Tribute Parameters

Entry Tribute: 2%

Exit Tribute: 12%

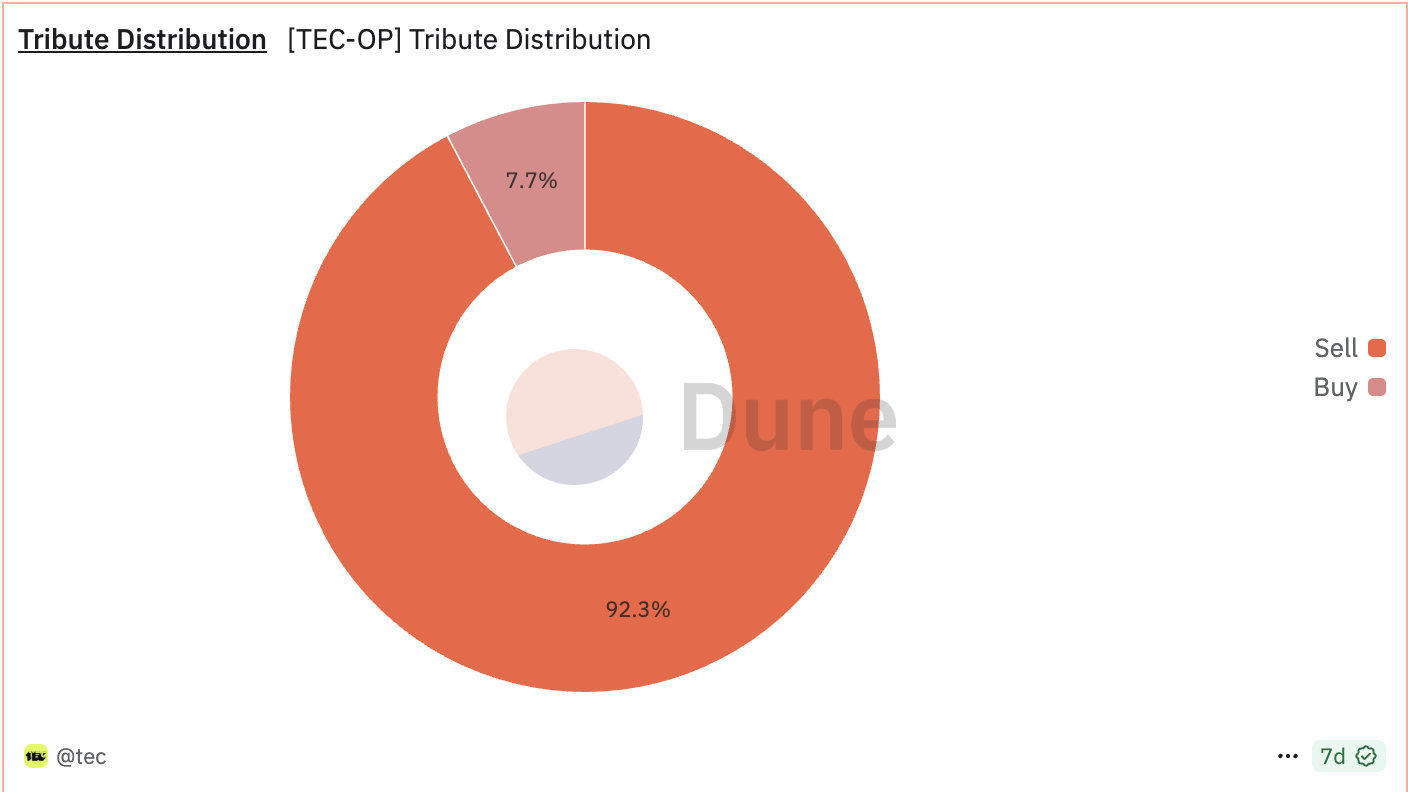

Total Tributes to the Common Pool since Migration: $25,235 (≈ 7.89 rETH)

Tribute Split: 92.3% from Exits (7.29 rETH) / 7.7% from Entries (0.60 rETH)

Tributes are a core feature of the $TEC token economy, built into the mechanics of the ABC. On the surface, they function like transaction fees where small percentages are taken during token buys and sells and routed to the Common Pool.

Tributes also serve a strategic governance function. They act as soft incentives or disincentives, influencing how and when people interact with the bonding curve. A low tribute encourages onboarding and exit. A high tribute discourages short-term flipping and speculative dumping, but creates friction in onboarding. By adjusting these parameters, the community can shape the economic behavior around the token.

Currently, the majority of funds entering the Common Pool are driven by sell pressure into the ABC. The imbalance between funds derived from Entry and Exit Tributes within the ABC shows that the ABC is primarily functioning as an exit ramp rather than a sustainable entry point for new participants. However, this isn’t necessarily negative. The Common Pool is accruing funds from both sides, and during this time of contraction and stagnation, a high exit tribute has limited the amount of exit in our economy. The current tribute percentages need future revision, but the current strategy is to maintain them until secondary market liquidity is optimized and we begin to enter a period of expansion where we can once again lower the exit tributes.

Secondary Market on Velodrome

To evaluate the secondary market on its own terms, we need to look closely at the data. How much volume are we seeing? What is the slippage? Are these pools serving our users or creating friction? The following section offers a detailed assessment of liquidity on Velodrome, the implications of using non-ETH pairs like OP and GIV, and why a shift to a TEC/ETH pair may be necessary if we want this market to function effectively.

Two pools were created post-migration within Velodrome:

| Pair | TVL | Volume | Slippage Risk |

|---|---|---|---|

| $TEC/$OP | $4,211.79 | $62,325.73 | ~12% |

| $TEC/$GIV | $677.00 | $10,510.19 | Nearly Unusable |

The TEC/OP pair handles the majority of activity, but even modest trades face double-digit slippage due to shallow liquidity. The TEC/GIV pool, while mission-aligned, lacks depth and price stability.

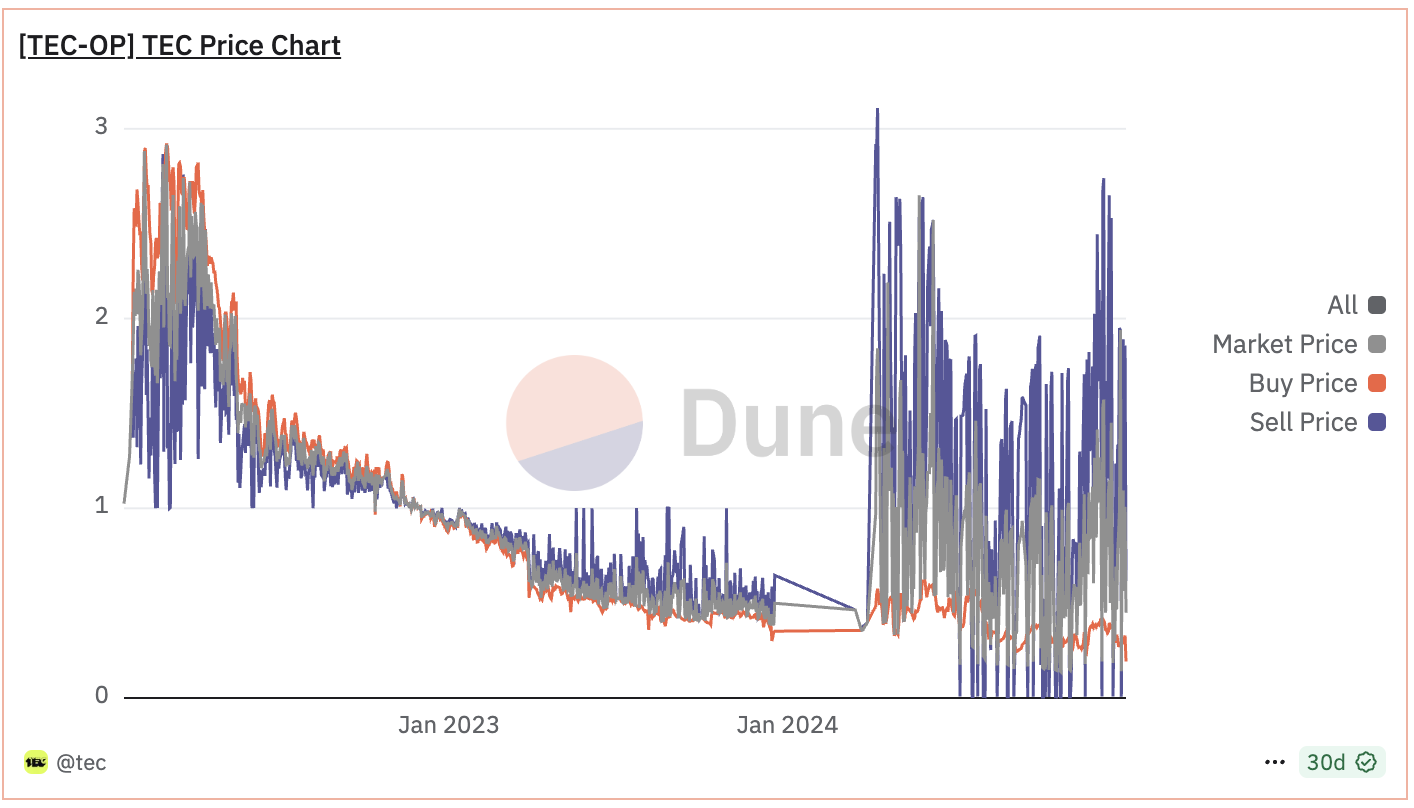

The price chart below shows the increasing volatility and divergence between buy/sell prices from LPs, especially after the migration. Our current Liquidity is insufficient to handle the transactions we are seeing. Without proper liquidity depth, the market becomes irrational, and users get penalized for interacting with $TEC on open markets. This is something we should address immediately.

ABC vs Secondary Market: Market Architecture Conflict

While the ABC offers a structured and mission-aligned approach to funding the Commons, it doesn’t operate in a vacuum. Since our migration to Optimism, we’ve also introduced a parallel liquidity route through Velodrome that offers public visibility and ease of use. However, maintaining both systems introduces tension.

One of the most unique and complex aspects of the $TEC token infrastructure is that we are currently operating these two very different types of markets simultaneously.

On the one hand, we have the ABC, which is the official entry and exit point for $TEC issuance and redemption. It is tightly integrated with our Common Pool and was designed to serve the economic goals of the TEC. Every interaction with the ABC generates funding for the Common Pool through tributes. It is not just a trading interface, but our primary funding mechanism.

On the other hand, we also operate a Secondary Market through Velodrome, a native DEX on Optimism. This market offers a familiar and user-friendly interface, fast execution, and visibility on token aggregators and dashboards. It gives us access to a broader public market and removes friction for casual traders or newcomers to the TEC economy.

At first glance, it might seem beneficial to offer both. But in practice, this dual-market setup has introduced real tension into the system. The two markets are competing for volume, but only one of them generates funding for the TEC. The secondary market draws in most of the trade volume because it is easier to access, but every trade that happens on Velodrome is a missed opportunity to earn tribute revenue for the Common Pool.

At the same time, the bonding curve charges a 12 percent exit tribute, which feels steep to many users, especially when token utility is still limited. For those trying to sell $TEC, the choice becomes either high slippage on Velodrome or high tribute fees on the bonding curve. In both cases, the user loses, and the token suffers.

Running two competing markets without a clear arbitrage strategy or coordination mechanism is leaving value on the table and in some cases, pushing users away entirely.

The key question is whether these two markets can complement each other, or whether we need to consolidate into one system that better serves both our funding goals and our user experience. This section lays out both sides of the tradeoff and frames the options we should consider.

| Market | Mechanism | Benefits | Drawbacks |

|---|---|---|---|

| PAMM | ABC | Generates funds to CP via Tributes | Poor UX, low discoverability |

| SAMM | Velodrome | High Visibility and good UX. | No revenue to Commons, suffers from slippage. |

Recommendations:

To address this, we propose three possible paths:

Option A: Close ABC to Public, Activate DAO Arbitrage

In this scenario, we would seek to close access to the Augmented Bonding Curve to the public, and establish an ACL for specific internal organizational wallets to use the ABC interface. This would mean all $TEC transaction volume would be on the secondary market. The TEC Organization would have sole arbitrage rights between markets and we could set Entry and Exit Tribute %'s to optimize for arbitrage gains and control of token supply. This would allow for us to generate funds for the Common Pool while bolstering our secondary market liquidity.

Requirements:

-

Bolster secondary market with sufficient liquidity.

-

Create ACL for ABC access

-

Lower Tribute %'s between 1-3% for both entry & exit.

-

Create an Arbitrage Bot between the markets that can be managed with low admin capacity.

Option B: Eliminate the Secondary Market

In this scenario, we would simply remove all secondary market liquidity, and force all transaction volume for $TEC to be routed through the ABC interface. This would mean that anyone interested in partciipating within the $TEC economy would need to acquire rETH, and purchase $TEC through the ABC.

Requirements

-

Sunset the Velodrome pools by removing the liquidity.

-

Set Tributes to modest 4-6% on each side.

-

Modify our custom UI to make further improvements for the ABC experience

Option C: Maintain dual-market structure, and gradually increase liquidity.

In this scenario, we maintain our secondary markets pools, making them more efficient over time. We also keep the ABC open to the public, and allow for open access to arbitrage between markets. This means we maintain the status quo more or less and seek to add more funds to the secondary market in hopes that it resolves the tension between markets.

Requirements:

-

Bolster secondary market with sufficient liquidity over time.

-

Maintain current Tribute %'s.

We propose migrating all current liquidity into a single TEC/ETH pool, and setting a clear target:

$15,000 minimum in TVL to bring slippage between 3-5%.

ETH is the most widely held asset in the ecosystem, and pairing TEC and ETH will:

-

Improve routing across DEX aggregators

-

Strengthen price discovery

-

Make $TEC more accessible to users outside the immediate community

For both Option A & C, we will need to take a structured approach for expanding and optimizing secondary market liquidity.

For Option A, we would need to provide this liquidity immediately as it would be the sole market for $TEC. For Option C, we can slowly build up the amount of liquidity over the next year.

The question is not whether we should have both markets, but whether we can manage them effectively.

Option A requires the Coordination team to serve as an active arbitrage agent and to manage the economy. Doing so provides a lot of benefits including our ability to control the supply of $TEC in a more granular way. Option A also requires costs to expand secondary market liquidity and to change the ABC smart-contract parameters.

Option B simplifies things entirely, but makes it largely inaccessible to new users. Users must acquire rETH prior to the purchasing of $TEC, and cannot take advantage of token routing mechanics within Velodrome.

Option C maintains the status quo with proposed iterative improvements. This option keeps both the ABC and Secondary Markets, keeps arbitrage open to the public, but faces the same limitations regarding driving funds to the Common Pool.

Pathways to Token Utility

The question of liquidity and price is important, but it’s only part of the equation. What ultimately determines the health of a token economy is whether people are using the token in ways that matter. Utility is what drives volume, creates reasons to hold and exchange the token, and generates meaningful economic flows through the bonding curve. This section explores the emerging utility paths for $TEC within our current initiatives.

In the coming months, we will have several promising opportunities to create new forms of utility and bring new life into the $TEC economy. Each of these represents a small but important exploration in possible pathways where $TEC utility can generate demand.

TEC Publishing Initiative

We are building a community-curated publication focused on token engineering, coordination, and regenerative crypto systems. $TEC could serve as the medium for tipping authors, voting on featured articles, or accessing curated content.

Virtual Conference and Events

We plan to host a virtual conference, with panel discussions, and talks from leading voices in different Web3 verticals. Tickets can be priced in $TEC, and speakers can be compensated directly in the token. This creates multiple transaction paths that route through the ABC and generate tribute income for the Common Pool.

TEC Grants Program Integration

As we evolve our grants program, we are exploring models where $TEC can be used to vote on proposals, delegate stake to project teams, or even unlock grant milestone payments through staking mechanisms. This not only deepens engagement but also introduces a layer of token-enabled accountability in funding decisions. The grant program will be the first area in which $TEC will have meaningful token utility, and we will begin to build our program around it.

Longer-Term Utility Experiments

There are also opportunities to embed $TEC in future coordination experiments. For example, we could develop reputation systems where $TEC is staked as a form of social signal, or create peer review and credentialing layers that require $TEC to access or validate knowledge. We could build ReFi-style coordination games, funding challenges, or bounties that require $TEC as an entry point. The potential is wide open, but it needs to be intentional.

The key point is this: utility is not something we wait for, but something we design. And now that the token architecture is functional, we are in the right position to begin prototyping small, high-impact use cases that get the token moving. Every time $TEC is used in a meaningful way, it reinforces the legitimacy of the token and creates more opportunities for tribute-based funding to flow into the Common Pool.

Closing Reflections

This report is not the end of the conversation, but the beginning of a much deeper one. We’ve outlined the current state of the $TEC token infrastructure, the strengths and friction points in our design, and the strategic decisions we now face. But where we go from here depends on the collective insight, creativity, and participation of our community. If you hold $TEC, you are a stakeholder in this system. We invite you to engage with these recommendations, challenge the assumptions, offer new ideas, and help shape the next chapter of the TEC economy. Whether it’s improving market architecture, expanding token utility, or rethinking our liquidity strategy, your input matters.